Regardless of your income, you can become financially independent. For starters, adopting a positive mindset can pave the path to financial fredom. I’ll show you how to live the lifestyle you deserve without breaking the bank.

What’s the secret to spending less and living well? Would you be surprised to learn that it all has to do with your mental health? As a therapist for over 20 years, I have worked in a variety of settings with a diverse array of clients. No matter who I was working with or their presenting issues, I noticed my clients were receiving unexpected bonuses due to their efforts in therapy. As they were making progress in therapy, they were receiving raises, promotions, starting successful businesses, and doing better financially.

Tips for Living Well and Spending Less

In therapy, no matter what issues you are working on, you are always simultaneously treating underlying feelings of self-worth, or the value you place on yourself. As my clients’ sense of worth improved, so did their finances—because of increased confidence, empowerment, assertiveness, and self-care. Scientists have observed a similar pattern in research literature; mental health significantly predicts future wealth, yet wealth does not affect future mental health. You can do the same by implementing four strategies to boost your mental health.

Learn to Love Yourself

While financial advisors help people manage their money, as a psychotherapist, I help professionals utilize psychological skills to improve their self-worth and emotional intelligence to achieve work-life balance and financial success.

Renowned author Suze Orman said in her book, Women & Money, “Lasting net worth comes only when you have a healthy and strong sense of self-worth.” However, Orman cautions that it doesn’t work the other way; having high net-worth doesn’t increase the likelihood that you will have high self-worth. Having greater self-worth reminds you that you deserve greatness.

Limit Impulsive Buying

When you limit impulsive buying, you have an opportunity to bulk up your pocketbook rather than deplete it. Thanks to the convenience of online shopping, with a click of a button you can order anything you’d like and have it conveniently arrive on your doorstep the next day. The convenience promotes impulse buying which is tough to reign in. The following are ways to limit your impulse buying:

Develop a relapse prevention plan

Identify the people, places, and things that are triggers for impulse buying. For example, the person you are trying to impress, the mall, or your retail apps on your phone. Make an effort to avoid those triggers and when you are faced with them, have a plan such as, call your therapist or sponsor, going for a walk, attending an online twelve-step meeting such as spenders anonymous, debtors anonymous, gamblers anonymous and more.

Consider a financial cleanse

Commit to a 7 to 21 day financial fast. This increases your spending awareness, and also saves you some cash. During your financial fast, do not use any credit cards, if possible, and do not go to any malls or retail stores. Delete retail apps on your devices and do not purchase any restaurant food or coffee—make everything at home and pay for your groceries in cash. If you need to get a gift for a friend, consider making them something, regifting an item you haven’t used, or being honest with them about your cleanse. This exercise will help you become more mindful of excess.

Spend Mindfully

For at least the next week (One-week minimum, lifetime practice recommended), keep a log of your spending. Before you spend money, ask yourself:

- Is spending money on this item or service absolutely necessary? If not, can I afford it?

- Will this expense bring me closer or further away from my personal, professional, and financial goals?

- Does it feel aligned with my values?

- Do I feel clear about this purchase in my gut?

At the end of the week, journal about anything you noticed such as spending less money because you were more conscious of it.

As you squelch your impulsive buying habits, you begin to build financial resilience.

Build Financial Resilience

Financial resilience refers to your ability to bounce back from adverse financial events, like losing your job, absorbing unexpected expenses, experiencing a decrease in work or business, a recession, pandemic, or losing money in an investment. According to financial expert Dave Ramsey, author of The Total Money Makeover, having good finances is like building a house. You need the right foundation in place (e.g., emergency fund, low or no debt), otherwise any sort of storm (adverse financial event) will knock it down.

Being able to rebound from a financial setback is directly proportionate to your financial health before the event. According to a 2017 report, 39 percent of Americans have zero money set aside and 57 percent have savings of less than $1,000. Therefore, two-thirds of Americans do not have financial resilience and could not withstand a major money challenge like what occurred for many during the COVID-19 pandemic. If you have little money saved, have lots of debt, and do not live by a budget, your recovery time is significantly extended.

Follow these best practices

- Budget

- Keep debt-to-income ratio low

- Live below your means by limiting your discretionary spending so you can save money

- Establish an emergency fund

- Pay down outstanding debt

- Stay the course with your investment strategy (not pulling funds when a recession hits)

Financial planners often recommend having enough savings to cover three to six months of expenses so that you can successfully move through hard times. Again, this can be established by reducing your variable, nonessential expenses. Consider having funds automatically transferred to your savings account or contributed to your investments on a monthly basis. Consider reading books such as The Latte Factor by David Bach and John David Mann or Financial Peace by Dave Ramsey to see how saving small amounts, like the price of a latte, can create significant financial improvement over time.

Related read: Tax Preparation Services Near Me

Savings should be kept liquid in a savings account, money market, or short-term CD where you have easy access to it if and when you need it. Once you have that in place, you may look at investing more in your future through retirement plans, college funds, or buying a home and paying down the mortgage. You might consider diversifying your investments to increase your financial resilience. For example, if all your savings are invested in your house, you may not be financially resilient if the housing market crashes. However, if you have invested in your home as well as mutual funds or CDs, you will have financial resources available during a housing market downturn. It’s a good idea to make sure your investments align with your values, so consider socially responsible investing—for example, in companies that are focusing on creating environmental sustainability. Doing so contributes to the resilience of our global community.

Recognize that Personality Traits Drive Our Spending Habits

Deep-rooted personality issues may cause us to spend more. For example, those with Narcissistic Personality Disorder suffer from grandiosity and may feel entitled to spend beyond their means. Others with Borderline Personality Disorder may feel positively empty at times and turn to spend as a means to fill themselves. How can certain personality traits (such as security and pleasure) impact a person’s want to buy and ability to control these impulses? People who have codependent tendencies and want to take care of others may feel compelled to spend resources to meet the needs of loved ones.

Those with controlling tendencies may want to buy clothes or decorative items for their loved ones because they want them to look or appear a certain way. Individuals who are less confident and secure in themselves are more susceptible to targeting advertisements. Pleasure seekers and those who want instant gratification are more likely to spend their money impulsively.

Those who are more fear-based, skeptical, or miserly may hoard their money and not be prone to spending. They take care of other family member’s problems, often to relieve their own anxiety. They tend to experience guilt and are prone to codependency and detrimental caretaking at their own expense. And, they may work in helping professions as a therapist, nurse, or paramedic. Overall, helping professionals do not realize their true earning potential as they tend to view their finances as being outside of their control and accept the notion that they will not make much money.

Related read: Can You Retire at 62 With 300k

Living Well and Spending Less: FAQ

In my practice, I often get asked for tips on achieving financial independence. The following are some of those questions.

How can I spend less and live more?

Reassess your values and prioritize spending on what is important to you. A life vision includes your personal and professional plans for the future. I’ve been awed and inspired by countless clients who’ve empowered themselves to radically recreate their life into something they never thought possible. You can do this too! As you continue to align your life and work with your core values, your vision begins to shine. Our vision is not a destination, it is a path. As we move forward, we see new horizons, perhaps more beautiful and expansive than we ever knew existed. And as we charter new frontiers, we can lead others along the way.

Having a life vision is always important, but it is invaluable when you are starting out on your journey, realizing that something in your life isn’t working and needs to change, or you identify a need in the world and want to be part of creating positive change.

For me personally, as I began to practice yoga and meditation more regularly, I noticed powerful changes. My mode of operation shifted from manic to more mindful and from a state of constant flight to more groundedness. Through mindfulness and walking meditations, I developed a renewed appreciation for nature. By quieting my mind-chatter, I noticed the beauty of the sky, trees, and flowers. I became less stressed and calmer, less reactive and more intentional as I connected with the peace and serenity that was available from deep within myself. As I became physically stronger, I was better able to handle work. If I was experiencing discomfort, I knew I could focus on my breath to help me move through the challenge. Because I was more present, virtually all of my relationships were improving and deepening.

How can I be happy with little money?

Focus on internals and not externals. Self-worth is internal. In psychology, our “locus of control” is the degree to which we believe we have control over the outcome of our life, as opposed to external forces beyond our control. From a financial perspective, this is a belief that we have the power to become rich even if we weren’t born that way or aren’t financially healthy now. Shifting to an internal locus of control is empowering and is strongly linked to high self-esteem.3

Healthy self-esteem is halfway between what I call Diva and Doormat. Dudes can be Divas too (or Divos, if you prefer). Divas are entitled and not respectful of other people’s boundaries and Doormats aren’t respectful of their own. Many believe people with big egos are grandiose Divas, but ego also causes people to be Doormats. This happens when your ego tries to protect itself by avoiding criticism, failure, or even the pressures and additional exposure that come with success. It might appear that Divas have self-esteem that is through the roof, but this is just a peacock facade to hide low self-esteem. To function as your most successful self, you need to make sure your ego isn’t causing you to veer towards Diva or Doormat.

Working with Divas in therapy requires me to build up their self-esteem and chip through layers of defenses. Because Divas have narcissistic tendencies, they are prone to grandiosity, materialism, and compulsive buying. Working with Doormats involves helping them see how not valuing themselves has negatively impacted their finances and supporting them in becoming more assertive.

How do you shop less and save more?

Curiously enough, the basics of money management is not rocket science—set a budget, make more than you spend, have a savings account, pay off your debt, and plan for the future. It’s our psychology that can make our financial lives difficult. Popular radio host and author, Dave Ramsey believes that financial success is 20 percent financial knowledge and 80 percent behaviors. He admits that financial success is all about your ability to control the person in the mirror. If you work the program in my book, The Financial Mindset Fix: A Mental Fitness Program for an Abundant Life, you’ll begin to see how your thoughts, feelings, attitudes, self-care, goals, motivation, and support impact your finances directly. Self-love is a big factor in your financial success.

How can I spend less on entertainment?

Consider low-cost ways to socialize and date. Instead of meeting your friends at an expensive restaurant, host a potluck and game night. When planning romantic outings with the object of your affection, consider activities that are free or low cost like heading to a park for a picnic or going on a bike ride adventure, or making a meal together at home. Public library cards are free and can provide lots of entertainment. You can even rent audiobooks or movies. Without shame or apology, have assertive conversations with friends and family where you set financial boundaries. You must care enough about yourself and your financial wellness to clarify expectations with others so they can help adjust expectations and reduce any pressure to overspend that you may be experiencing.

In my practice, many of my clients have reported because of the pandemic how much money they have saved by not going out to restaurants or bars, canceling gym memberships, not going to the salon, and more. They’ve reported greater financial awareness of how they may have previously been overspending and how it feels better to have some cushion in their bank accounts.

How can I spend less on shopping?

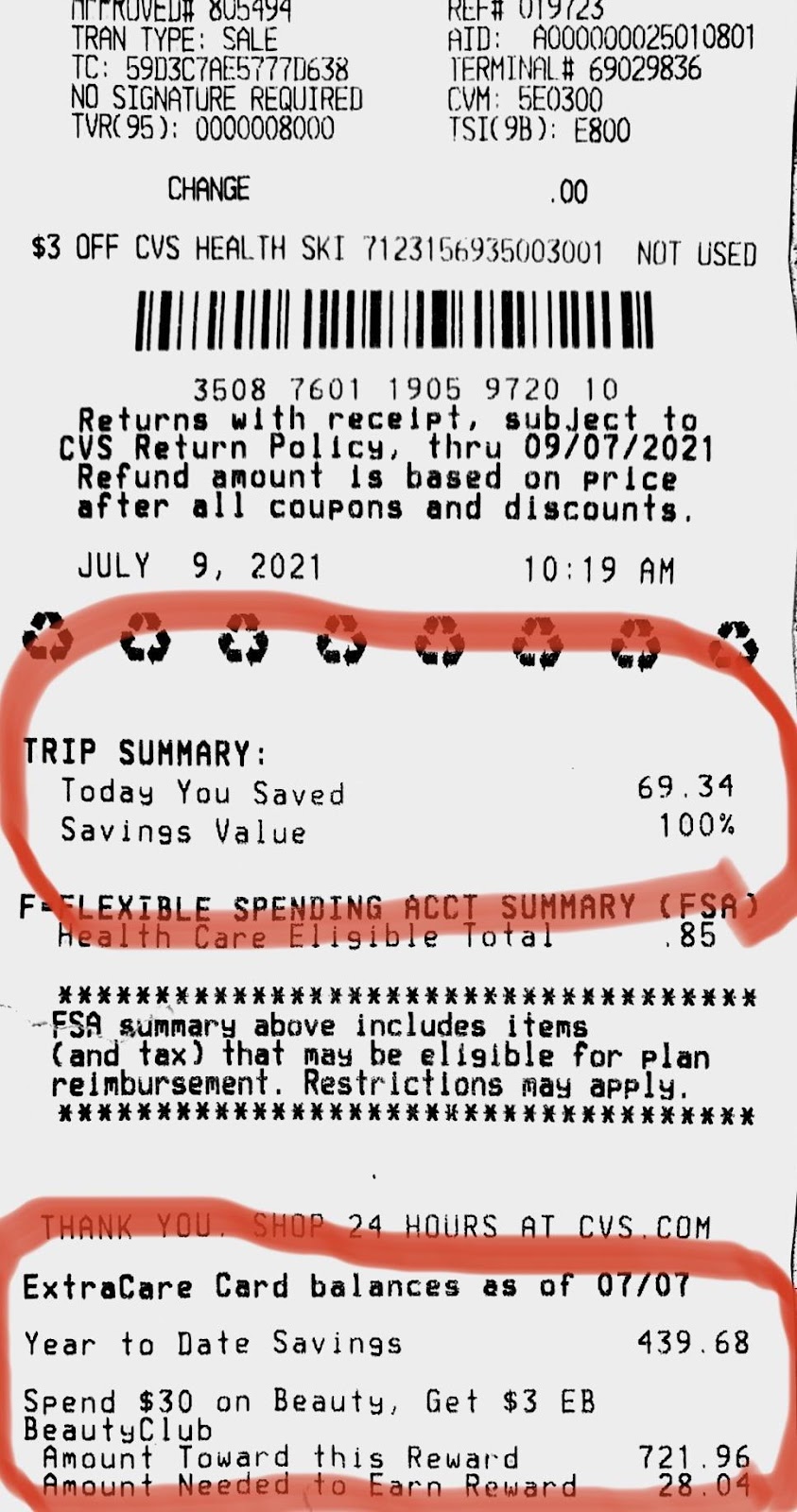

This is an actual receipt from CVS where I bought nearly $70 of merchandise and paid 85 cents because I am a huge couponer. I recommend:

- Downloading the apps of the stores you most frequently shop

- Using coupons

- Being loyal to a brand (CVS or Walgreens, for example) so you can maximize your rewards

- Always searching for promo codes before purchasing online

- Using sites such as Groupon or Honey for savings

- Writing a shopping list and sticking to it

- Having an accountability partner

- Shopping with cash, not credit cards

Final Thoughts

Being financially independent at a young age provides a lot of freedom. You don’t need to stay at a job you hate simply because you need the money. By taking care of your mental health, you are paving the path toward financial independence. As you begin incorporating some of these tips into your life, you’ll see it’s possible to live well and spend less.